6 Essential Cyber Insurance Requirements Your Business Needs to Meet

Table of contents

Cyber incidents are a growing concern for businesses of all sizes, and the financial impact is often devastating––IBM found that the global average cost of a data breach in 2024 was USD 4.88 million, a 39% increase since 2020.

But one thing that remains consistent?

The need for robust protection against the fallout of cyberattacks is more critical than ever.

With ransomware, data breaches, and network security incidents becoming more frequent, companies must now prioritize cyber liability insurance to safeguard their operations and mitigate losses.

Ahead, we’ll break down what cyber liability insurance covers, why it’s become indispensable for businesses in 2024, and the key steps you need to take to meet cyber insurance requirements. We’ll also share tips for navigating rising premiums and increasing coverage demands.

What is Cyber liability insurance?

Cyber liability insurance is a policy that helps businesses manage the fallout from cyberattacks, including covering costs related to data breaches, system hacks, or theft of sensitive customer data.

It typically covers:

- Legal fees and expenses if your business is sued due to a cyberattack.

- Credit monitoring services for impacted customers.

- Costs of notifying customers or stakeholders about breaches.

- Recovery costs, such as restoring computer systems or data.

- Ransom payments in some cases of ransomware attacks or cyber extortion (depending on the policy).

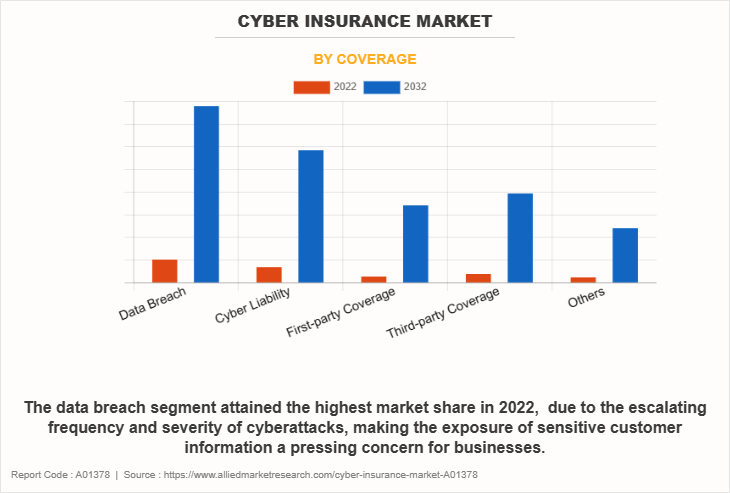

Cyber liability policies are typically divided into first-party and third-party coverage:

- First-party coverage addresses losses to your company directly (e.g., system repair, recovery, and response costs).

- Third-party coverage helps cover claims made against your business by customers, vendors, or partners who are affected by the cyber incident.

Is cyber insurance mandatory?

As of 2024, cyber insurance is not universally mandatory, but in some industries and jurisdictions, regulations are increasingly pushing for its adoption.

Highly regulated sectors like healthcare and finance are seeing more stringent requirements due to the sensitive nature of the data they handle. Laws like the GDPR (General Data Protection Regulation) in Europe, and frameworks like HIPAA in the US, have placed a heavier emphasis on ensuring that organizations manage the risks of data breaches, which in turn is driving cyber insurance adoption.

In countries like Germany and the United States, certain businesses working with government contracts or critical infrastructure may be required to have cyber coverage.

Why are some insurers and brokers advocating for government intervention in the Cyber Insurance Market?

As cyberattacks grow in frequency and severity, some insurers and brokers, including Zurich and Marsh McLennan, have been vocal about the need for government intervention to stabilize the cyber insurance market.

“Both the insurance industry and the public sector are urged to collaborate, share, and innovate to confront the growing cyber risk protection gap, foster resilience, and safeguard our society and economy from the escalating cyber threat landscape,” the report said. “Strengthening society’s cyber resilience is inextricably linked to the evolution of the cyber insurance market.”

The increasing costs of claims are leading to concerns that the insurance market alone cannot sustain the financial burden, especially in cases of catastrophic events (e.g., large-scale infrastructure attacks).

Government involvement could help create a public-private partnership that would provide reinsurance or financial backstops for insurers, ensuring that businesses remain protected while the market remains viable.

What do growing financial losses mean for cyber insurance requirements?

According to recent reports, the financial losses from cybercrime are projected to reach $10.5 trillion annually by 2025, showing a dramatic rise from previous years.

These losses are driving higher premiums for cyber insurance products as insurers face increased payouts from frequent, high-cost attacks like ransomware and cyber extortion. Businesses are also finding it more difficult to secure comprehensive coverage due to rising costs and more rigorous underwriting standards

Financial regulators and lawmakers are starting to explore new frameworks to ensure that businesses remain protected as cyber insurance becomes a critical element of risk management, potentially leading to further regulatory requirements around insurance.

Risk assessments are becoming more critical, and insurers are now examining the security controls businesses have in place to mitigate these rising threats more closely.

6 key cybersecurity insurance requirements

Most insurance service providers have some requirements businesses must follow to ensure their coverage is valid. Here are the top six requirements you’ll likely need to adhere to:

1. Roll out cyber training

Cyber training for employees is one of the most critical requirements for cyber insurance. Insurers often look for proof that a business is taking proactive steps to educate its workforce on common cyber threats such as phishing, ransomware, and apps used to bypass security measures.

Why it’s important: Human error remains a leading cause of data breaches, and regular training can significantly reduce the likelihood of an incident occurring due to a staff mistake.

What insurers expect: Cyber insurance providers typically require that businesses conduct annual or biannual training, covering how to recognize suspicious emails, secure passwords, and report potential security incidents. Implementing security awareness programs will strengthen your claim eligibility and may even lower premiums.

2. Implement identity access management (IAM)

Identity access management ensures that the right individuals have access to the right resources at the right times, using strict authentication processes like multi-factor authentication (MFA) to control who can access sensitive data or systems.

Why it’s important: Proper IAM prevents unauthorized access to your networks, reducing the risk of data breaches caused by compromised credentials. Insurers will want to see that your organization has a strong system in place to control access to sensitive data.

What insurers expect: You’ll need to implement IAM tools that provide real-time monitoring, role-based access controls, and secure authorization processes. Multi-tiered verification methods, such as biometrics and single sign-on (SSO), are also highly encouraged. These tools are crucial to meet cyber insurance requirements for identity and access controls.

3. Uphold regular data backups

Regular data backups are critical for maintaining business continuity after a cyberattack. Many policyholders require businesses to back up their data frequently to ensure that vital data is not permanently lost in the event of a ransomware attack or system breach.

Why it’s important: Backups help businesses restore data quickly without having to pay ransoms or face extended business interruption or downtime, which are critical factors in reducing potential losses.

What insurers expect: Insurers often require businesses to back up their data at least daily and store it in a secure, off-site location, to avoid omissions in incident response plans. Backups should be encrypted and regularly tested to ensure they can be restored efficiently in case of an emergency.

4. Enforce data classification

Data classification involves organizing and categorizing your business’s data based on its level of sensitivity. This helps ensure that high-value or sensitive data receives the highest level of protection, while less critical information can be handled with fewer restrictions.

Why it’s important: Without clear classification protocols, sensitive data could be inadvertently exposed or poorly secured, leading to more severe consequences during a security breach. A breach involving highly sensitive data can lead to greater financial loss and reputational damage, which insurance companies want to mitigate.

What insurers expect: A clear data classification policy is essential to ensure cyber coverage remains valid, particularly when it comes to handling sensitive personal data and intellectual property. Insurers look for businesses to have clear, documented data classification policies that identify sensitive data like personal customer information, financial records, or intellectual property. Access to this data should be limited and protected with encryption.

5. Implement multi-factor authentication

Multi-factor authentication is a security protocol that requires users to provide two or more verification factors to gain access to an account or system.

Why it’s important: MFA adds an additional layer of security, significantly reducing the likelihood that cybercriminals can access systems or accounts using compromised passwords alone. It’s one of the most effective ways to prevent unauthorized access.

What insurers expect: Cyber insurance providers typically require MFA to be enabled for all critical systems, especially for administrator accounts and any access to sensitive data. Methods like SMS codes, authenticator apps, or hardware tokens are common ways to meet this requirement.

6. Use a preventative EASM cyber security solution like CybelAngel

External attack surface management (EASM) solutions, such as CybelAngel, are designed to continuously monitor the digital footprint of your business and detect any potential vulnerabilities or exposed assets that attackers could exploit.

Why it’s important: EASM tools provide a proactive approach to identifying risks before they can be exploited, helping businesses to prevent cyberattacks rather than just reacting to them. This level of visibility is crucial for minimizing exposure and enhancing the security posture of a company

What insurers expect: Cyber insurance providers increasingly look for businesses to have preventative measures in place that can detect and mitigate risks in real-time. Businesses using an EASM solution like CybelAngel demonstrate a strong commitment to risk mitigation, positively impacting cyber insurance premiums, pricing and coverage terms.

Cybersecurity insurance requirements FAQs

1. What types of businesses need cyber insurance the most?

Businesses that handle sensitive customer data (e.g., finance, healthcare, ecommerce) or operate in industries that rely heavily on technology infrastructure are at the greatest risk. They should prioritize having comprehensive cyber insurance.

2. What are the minimum requirements for cyber insurance coverage?

Most policies will require that companies maintain basic cybersecurity measures like firewalls, regular software updates, and employee training on phishing and other cyber risks. Without these security controls insurers may refuse coverage or deny claims.

3. Does cyber insurance cover ransomware payments?

Some policies may cover ransomware payments, but many insurers are now either limiting or completely excluding these types of claims due to their high frequency and cost. It’s important to check the specific terms of your cyber insurance policy.

4. What happens if my claim is denied?

Common reasons for denied claims include failing to meet basic security protocols, not disclosing critical risks to the insurer, or violating policy terms. Ensure that you comply with all stipulations in the policy to avoid this situation.

5. How is the scope of coverage determined?

The scope of cyber insurance coverage is typically determined by assessing a business’s risk exposure. Insurers will look at factors like the volume of sensitive data managed, existing cybersecurity measures, and the company’s history of cyber incidents.

Wrapping up with some cybersecurity tips

In 2024, businesses can no longer afford to ignore the importance of cyber liability insurance. To make sure your business is fully protected:

- Conduct regular cyber risk assessments to identify vulnerabilities and update your incident response plan.

- Implement strong security controls, such as MFA and EDR software, to reduce your exposure.

- Review your policy’s exclusions to understand your cyber coverage and limitations.

- Stay informed about changes in cyber insurance products and evolving regulatory requirements.

With the right cybersecurity best practices, you can protect your organization from external risks and lower your cybersecurity insurance premiums.

Ready to protect your company and reduce your insurance cost? Request a demo today.

About the author